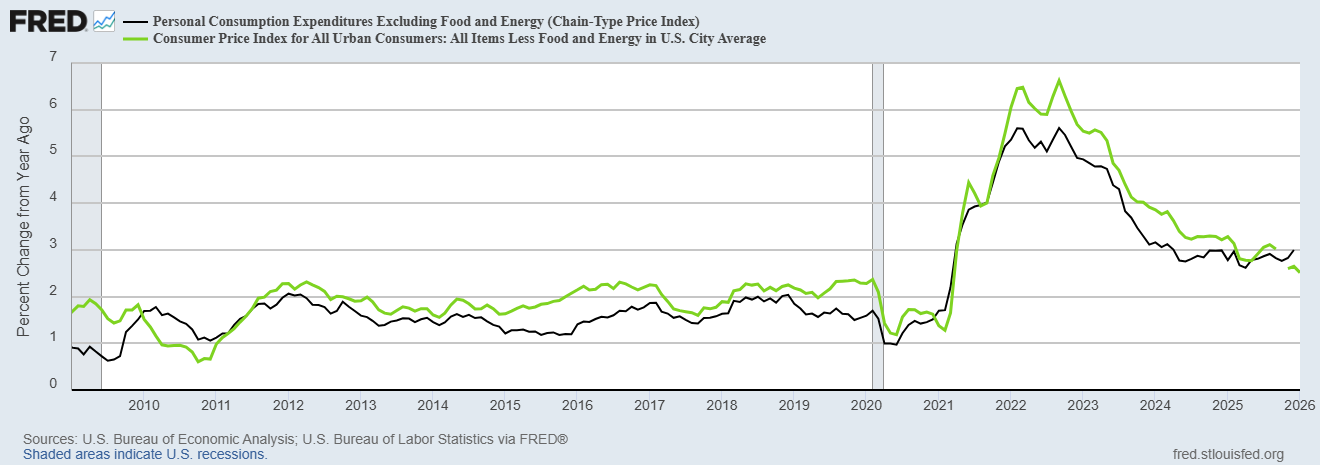

The Personal Income and Outlays for December, 2025 from the Bureau of Economic Analysis (BEA) included some bad news for inflation. The latest tariff chaos unfortunately drowned out the alarms. The Federal Reserve’s preferred measure of inflation, the Personal Consumption Expenditures (PCE), diverged from the more benign picture from the CPI and increased 2.9%. The core PCE increased 3.0% year-over-year. Core PCE has now crossed core CPI. This rare event last happened at the beginning of the pandemic-era inflation. While there is little reason to believe inflation is at the beginning of such a resurgence, my inclination to worry about inflation just went into overdrive over this image.

Services was the biggest driver of December’s core PCE with a 3.5% year-over-year jump. Services has been a consistent contributor to inflation’s stickiness. The biggest components within services were housing and utilities, recreation services, and financial services and insurance. Each of these components were also top drivers of services PCE inflation a year ago, so I fully expect them to continue to remain elevated…and worrisome.

Why Does the Fed Prefer PCE over CPI?

The general public and financial media pay much more attention to the CPI than the PCE. So it is easy to understand how a hot PCE number got little attention among the tariff headlines. However, the Fed cares more about PCE because it is a more comprehensive measure of inflation than the CPI. The PCE relies on business surveys that include expenditures made on behalf of consumers. In an explainer, the BEA provides the following example:

“For example, the expenditure weights for medical care services in the CPI are derived only from out-of-pocket expenses paid for by consumers. By contrast, medical care services in the PCE index include those services purchased out of pocket by consumers and those services paid for on behalf of consumers—for example, medical care services paid for by employers through employer-provided health insurance, as well as medical care services paid for by governments…”

This distinction is particularly important since the Fed spends a lot more time talking to businesses (like in the Beige Book) than to consumers.

Gold probably got both messages: sticky/heating inflation and fresh economic chaos. The SPDR Gold Shares (GLD) bounced perfectly off support at its 20-day moving average (DMA) (the dashed line) and followed through with a 2.7% gain to start the trading week.

Be careful out there!

Full disclosure: long GLD calendar call spread