Federal Reserve Chair Jerome Powell made a timely appearance in Amsterdam for a meeting of the Foreign Bankers’ Association. It was the day before the release of the April CPI report, so Powell’s commentary set the stage and an immediate context for interpreting the April results. Powell expressed no enthusiasm for rate cuts, but he also insisted that monetary policy is currently restrictive. So when the April CPI came in “softer than expected”, the relief in the market was palpable: rate cuts are (presumably) still on the table this year. The S&P 500 (SPY) and the NASDAQ (COMPQ) made new all-time highs and validated my bullish call from last week.

I break down the key components of Powell’s observations (using the transcript from the CNBC TV recoding of the live event) and then juxtapose them with the prospects for inflation going forward.

The S&P 500 (SPY) since the October lows overlayed with my past short-term trading calls. (Source: Tradingview.com)

Is Policy Really Restrictive?

Powell observed that “the labor market is about as tight as it was before the pandemic in 2019, and that’s good. Real wages are now positive, and unemployment has been below 4% for 27 consecutive months, something that hasn’t happened in half a century. So, the labor market is very strong, with signs of gradual cooling and rebalancing, so that the supply and demand for workers are coming back into balance, just as we would want.” The logic did not make sense at first. Powell provided the evidence of balance in the labor market later on in the discussion. He noted that “the ratio of vacancies to unemployed people, for example, has gone from more than 2 to 1 to now 1.3 to 1, and it was 1.2 before…You also see wages coming down, and you see quits coming down.” Most importantly, Powell used these observations as evidence that “policy is probably restrictive.”

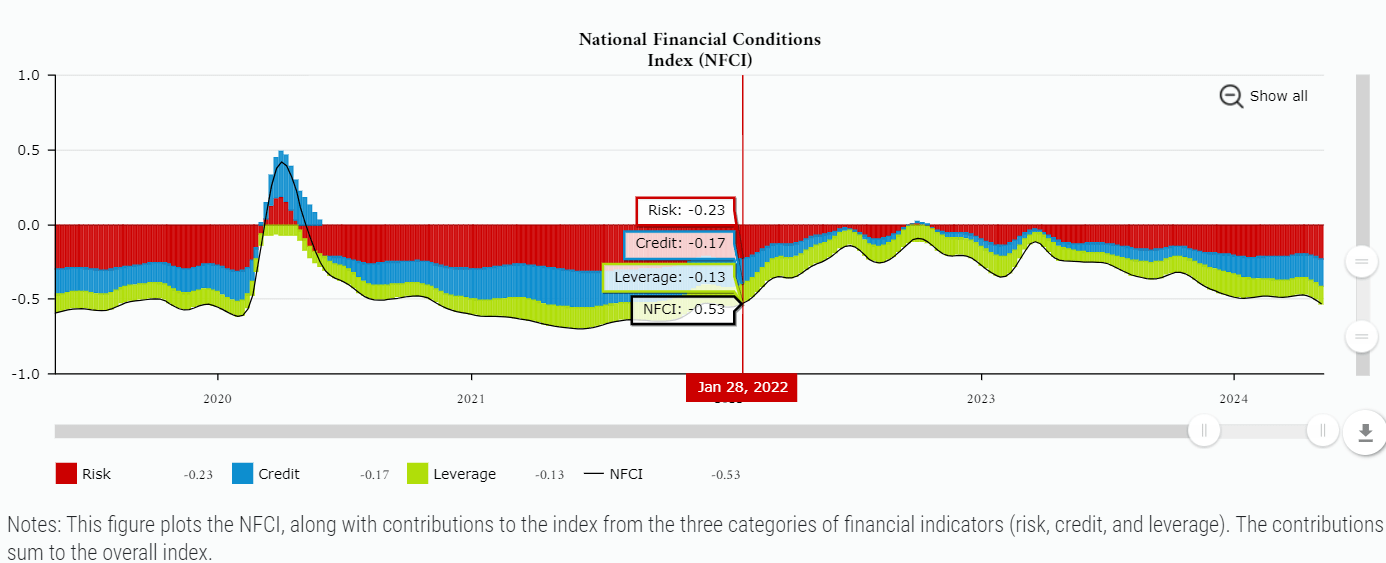

Powell went on to add that restrictive policy is weighing on rate-sensitive spending. However, the conventional indicators of financial conditions still show they are just as loose as they were before the Fed started hiking, January 28, 2022 to be exact. In other words, either the market has done some serious advanced front-running of rate cuts or current policy is not nearly as restrictive as the Fed thinks. Even the stock market’s all-time highs suggest monetary conditions are not tight. From the Federal Reserve Board of Chicago’s National Financial Conditions Index (NFCI) (follow the black line for ANFCI):

Even the hand-wringing this year from the Federal Reserve about resilient inflation implies that policy may not be restrictive enough (whether that means rate hikes, or, more likely, extending the time horizon for current rates).

Resilient Inflation

Powell repeated a familiar refrain about inflation not falling as fast as expected given presumed restrictive policy. Thus, Powell had to show deference to the possibility that today’s high rates will need to stay in place longer than expected:

“The first quarter in the United States was notable for its lack of further progress on inflation. We had higher readings in the first quarter, higher than we expected. We did not expect this to be a smooth road, but these were higher than I think anybody expected. So, what that has told us is that we’ll need to be patient and let restrictive policy do its work.”

This comment tells me rate cuts are nowhere on the horizon. Moreover, Powell noted “we have the highest interest rates in some time. It may be that it takes longer than expected to do its work and bring inflation down.”

Most telling were Powell’s words when a question offered the opportunity to reassure the market that rate cuts were still on the way. Emphasis mine:

“So, as I just mentioned, I do think it’s really a question of keeping policy at the current rate for a longer time than had been thought. By many measures, the policy rate is restrictive. The question is, is it sufficiently restrictive? And I think that’s going to be a question that time will have to tell. Entertain the possibility? That could be a very small probability, but I have said that I don’t think it’s likely based on the data that we have that the next move we make would be a rate hike. I think it’s more likely that we’ll be at a place where we hold the policy rate where it is.”

Note what Powell did NOT say: it’s more likely that rates will be lower by the end of the year (or even next year).

So, nowhere in the discussion did Powell provide a line for the market expect rate cuts anytime soon. Thus, he has primed the market to get excited about any soft data that could provide the seeds of an excuse for the Fed to cut rates. Powell’s positioning is made even more potent by the stock market’s ability to trade at all-time highs despite all the hand-wringing about inflation this year.

Inflation Forecast

Powell expressed a lot of uncertainty about the path for inflation despite his confidence that “we will do that, that we will get inflation down to 2%.” I am not sure how rate cuts help bring down inflation (Turkey sure learned a central bank cannot cut rates to lower inflation), so I have to assume Powell has an image of “higher for longer” monetary policy rates.

Responding to a question on whether inflation could end up being more persistent than expected, Powell said: “I think we need more than a quarter’s worth of data to really make a judgment on that.” It’s like the perpetual data delay. It will be interesting to hear whether April’s inflation data finally gives the Fed more confidence that inflation is coming down sustainably. Time is running out for the Fed to start telegraphing the first rate cut, so the pressure is on the Fed to spin a story about April and May inflation that points to the 2% target.

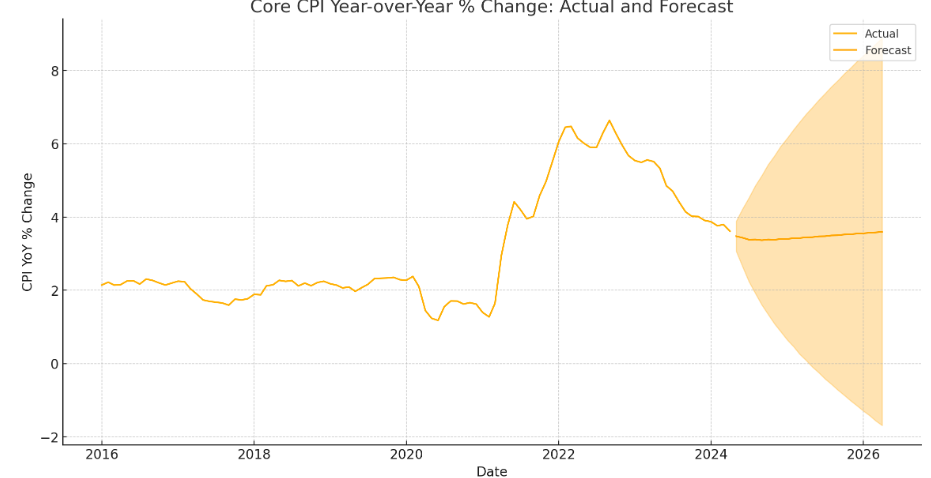

When I look a the core CPI graph (year-over-year percentage change in the price index), it looks like inflation will soon resume a steep descent. To apply a modicum of extra rigor, I ran a simplistic forecast through ChatPGT’s Data Analyst. I let the model pick its forecasting method. This is a very simplistic forecast because it only uses the aggregate CPI time series. A more accurate forecast would consist of aggregating the forecasts of individual components of core CPI.

I provided the model core CPI (measured year-over-year) data back to 2016. I wanted the model to surmise that “equilibrium” consists of a tight range for inflation. I did not provide any more data because I figured the further away history gets from the pandemic era, the less likely the model has any value (another downside of using a single, aggregated time series for the forecast).

The chart below combines the actual core CPI data with the forecast. The “funnel” around the forecast shows the confidence interval within which inflation will fall in the future at 95% certainty. The wide swath of possibilities is consistent with Powell’s uncertainty about the path ahead. The flat average forecast is a typical behavior of time series forecasting where there are no definitive seasonal effects detected or modeled future episodic events. (For you ChatGPT and statistics wonks, I provide an Appendix below where ChatGPT explains the model and justifies its approach).

Source: U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items Less Food and Energy in U.S. City Average [CPILFESL], retrieved from FRED, Federal Reserve Bank of St. Louis; May 15, 2024.

The Bond Market Rules

Putting aside vain attempts to forecast future inflation, the bond market is the ultimate arbiter of inflation expectations and/or how inflation may impact interest rates. The bond market in the form of the iShares 20+ Year Treasury Bond ETF is at a very critical (technical) juncture. The downtrend in TLT (uptrend in rates) was the ultimate guide in pushing the market into its April correction. The rebound in stocks for May perfectly correlates with the rebound in TLT (lower rates). The “soft” April CPI report sent TLT up 1.4% and right up against the top of the downtrend channel.

iShares 20+ Year Treasury Bond ETF (Source: TradingView.com)

A confirmed breakout with a higher close should open the floodgates of bullishness for the stock market. A failure at resistance from the upper part of the channel could trigger a false breakout for the indices. Thus, given this year’s correlation with stocks, I reloaded on TLT puts as a hedge on my long trading positions.

Overall, the lesson in all these dynamics is that inflation combined with the interest rate response should continue to dominate the market’s underlying narrative. With rates on hold, even the Fed is just along for the ride for now.

Be careful out there!

Appendix (ChatGPT explains and justifies the CPI forecast)

{the following is verbatim including ChatGPT’s musings on data types and fixing its own processing problems}

The data consists of monthly core CPI year-over-year percentage changes starting from January 2016. To project the CPI for the next 24 months, I will use the ARIMA (AutoRegressive Integrated Moving Average) model, which is well-suited for time series forecasting.

Justification for ARIMA Model:

- Handling Trends and Seasonality: ARIMA can model both trend and seasonality in the data, which is crucial for accurate CPI forecasting.

- Flexibility: The model can be adjusted to different time series characteristics through its parameters.

- Proven Effectiveness: ARIMA has been widely used and tested in economic and financial forecasting, making it a reliable choice.

Steps for the Analysis:

- Data Preparation: Convert the date column to a datetime format and set it as the index.

- Stationarity Check: Perform tests to check if the time series is stationary. If not, apply differencing.

- Model Identification: Use autocorrelation (ACF) and partial autocorrelation (PACF) plots to identify the order of the ARIMA model.

- Model Estimation: Fit the ARIMA model to the data.

- Forecasting: Generate forecasts for the next 24 months.

- Confidence Intervals: Calculate confidence intervals for the forecasts.

- Visualization: Plot the actual data, the forecasted values, and the confidence intervals.

Let’s start with the data preparation and initial analysis.

The Augmented Dickey-Fuller (ADF) test results are as follows:

- ADF Statistic: -0.988

- p-value: 0.758

- Critical Values:

- 1%: -3.508

- 5%: -2.895

- 10%: -2.585

Since the p-value is greater than 0.05, we fail to reject the null hypothesis that the time series is non-stationary. This indicates that the series needs to be differenced to make it stationary.

Let’s apply first-order differencing and recheck for stationarity.

The ADF test results after first-order differencing are as follows:

- ADF Statistic: -2.447

- p-value: 0.129

- Critical Values:

- 1%: -3.509

- 5%: -2.896

- 10%: -2.585

The p-value is still greater than 0.05, indicating the time series is not yet stationary. Let’s apply second-order differencing.

The ADF test results after second-order differencing are as follows:

- ADF Statistic: -2.843

- p-value: 0.052

- Critical Values:

- 1%: -3.509

- 5%: -2.896

- 10%: -2.585

The p-value is now close to 0.05, indicating the time series is approaching stationarity. Since it’s marginally above the threshold, we will proceed with ARIMA modeling with second-order differencing.

Model Identification

Next, we’ll use ACF and PACF plots to identify the appropriate orders (p, d, q) for the ARIMA model.

The ACF and PACF plots provide insights into the appropriate orders for the ARIMA model:

- ACF (Autocorrelation Function): The ACF plot shows significant lags at various points, suggesting that an MA component (q) might be needed.

- PACF (Partial Autocorrelation Function): The PACF plot shows significant lags at the beginning, suggesting that an AR component (p) might be necessary.

Given the plots, an ARIMA model with orders (p, d, q) will be selected. Based on visual inspection, we can start with ARIMA(2, 2, 2) since both ACF and PACF show significance up to lag 2.

Model Estimation

Let’s fit the ARIMA(2, 2, 2) model to the data and generate forecasts for the next 24 months.

It seems there’s an issue with the data types in the forecast confidence intervals, which might be causing the error. Let’s inspect the forecasted values and the confidence intervals to identify the problem.

The forecasted values and confidence intervals appear to be valid. The issue might be due to incorrect data handling during the plotting process.

To resolve this, let’s explicitly convert the confidence intervals to a numeric type before plotting.

It appears the error persists despite converting the confidence intervals to float. This might be due to a mismatch in the indices of the forecast intervals and the forecasted mean.

To resolve this, I’ll ensure the indices of the confidence intervals match those of the forecasted mean before plotting.

The issue may be due to an incompatibility between the data types of the forecast index and the confidence intervals. To resolve this, I will ensure all data is in the correct numeric format and use the correct plotting function.

I’ll convert all relevant data to the same data type and then re-plot.

The plot now correctly displays the actual data, the forecast, and the confidence intervals.

Summary of Analysis and Forecast:

- Data Preparation: The time series data was checked for stationarity and transformed using differencing to achieve stationarity.

- Model Selection: Based on the ACF and PACF plots, an ARIMA(2, 2, 2) model was chosen.

- Model Fitting and Forecasting: The ARIMA model was fit to the data, and forecasts for the next 24 months were generated.

- Visualization: The actual data, forecasted values, and confidence intervals were plotted to provide a comprehensive view of the projected CPI.

This approach provides a robust forecast by incorporating both autoregressive and moving average components, accounting for trends and seasonality in the core CPI data. The confidence intervals offer a range of possible future values, helping to understand the uncertainty associated with the predictions.

Full disclosure: long SPY calendar call spread, long TLT puts

[…] Fed’s Powell Avoids Rate Cut Talk While April CPI Keeps Hope Alive → […]