“Tariffs are a one-time price adjustment.” This quote is the bold yet defensible claim U.S. Treasury Secretary Scott Bessent made during a CNBC interview this past week. Bessent is leaning on an inflation sleight of hand, but he is technically correct. The direct cost of a tariff passes through the system almost all at once. If an importer passes on the tariff to the consumer then that price increase will register in the CPI (Consumer Price Index) as an increase in the price level, aka inflation. The following year, all else being equal, the tariff does not increase the price level a second time. Thus, the tariff no longer contributes to inflation and becomes a one-time adjustment.

However, a systemic perspective greatly weakens claims of a one-time adjustment. Over time, tariffs can create a cascading effect through the economy, especially when tariffs are broadly applied across a wide swath of goods and services. Over time, tariffs can embed and entrench inflationary pressure in the economy from the following:

- Wage pressures – workers may demand higher wages to compensate for persistently higher consumer costs.

- Supply chain adjustments – companies may shift to more expensive domestic or alternative suppliers.

- Cost pass-through effects – producers adjusting pricing behavior in response to permanently higher costs as they enjoy greater pricing power amid a reduction in alternatives.

Moreover, successive rounds of tariffs, as the economy is experiencing now, amplify inflationary ripple effects, making them harder to unwind.

Still, that one-time adjustment is higher and persistent. So I am skeptical as Bessent also tries to resurrect “team transitory” when explaining the impact of tariffs. For inflation to be transitory, price levels would need to revert after the initial tariff shock. Tariffs make price reversion unlikely by locking in a permanently higher cost base unless offset by productivity gains, currency shifts, or supply chain innovations. Again, all else being equal, as long as the tariff is in place, someone is paying the cost, this year, the next year, and so on. The price increase will not disappear on its own accord. If you are still complaining about how much higher prices are now compared to 2019, you will find yourself complaining years out about the higher prices brought on by tariffs passed on to the consumer level.

Can pandemic-era inflation be described as a one-time adjustment? Of course. All we need to do is extend the time period over which “one-time” applies. The chart below shows the year-over-year change in the average annual CPI. Even if inflation slows to its pre-pandemic pace by 2026, the accumulated price increases remain, permanently raising the cost of living (of course, I have my doubts about the pace of inflation’s decline given the underlying stickiness of key inflationary components). In 2027, a casual observer could look back and conclude this inflationary era was a one-time price adjustment that lasted about 5 years. While the conclusion would be technically correct, the broad price level remains significantly elevated, straining household budgets long after the inflationary event passes. In other words, a “one-time adjustment” in this context is only academically meaningful.

Source: U.S. Bureau of Labor Statistics, Consumer Price Index for All Urban Consumers: All Items Less Food and Energy in U.S. City Average [CPILFESL], retrieved from FRED, Federal Reserve Bank of St. Louis; March 7, 2025.

Terms like “transitory” and “one-time adjustment” do not speak to the direct and real-time impacts on consumers. These terms are sleights of hand to convince financial markets to look through the price dynamics. Consumers cannot look through these impacts. They must immediately adjust spending habits to account for the deterioration in spending power from tariffs, especially broad based ones (all else being equal).

Adjustments and Transitory Effects In Currency Markets

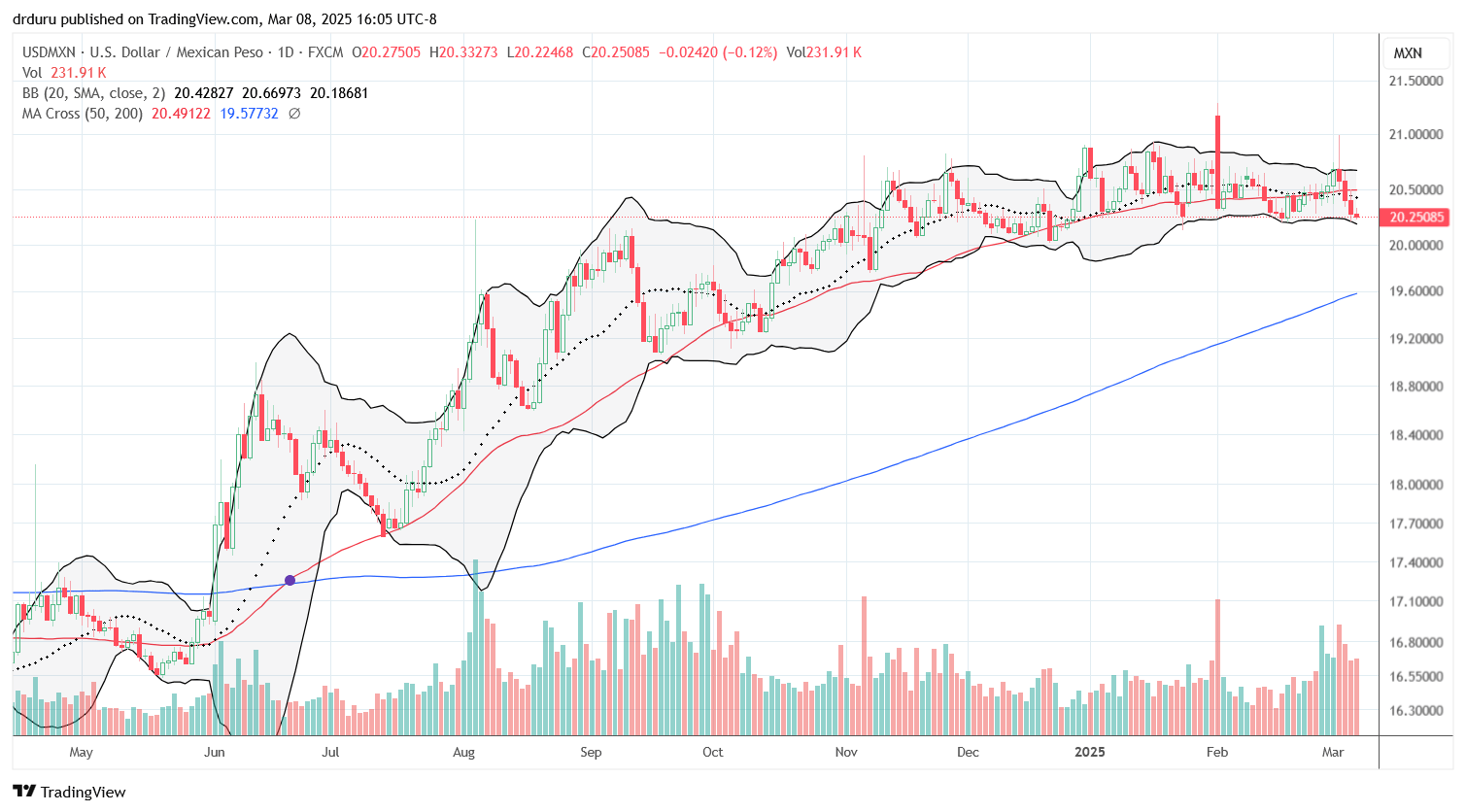

In foreign exchange, the Canadian dollar and the Mexican peso have served as ground zero for the current chaos over ever-changing policies on tariffs and economic warfare. However, overall, against the U.S. dollar, these currencies have stuck to a well-defined trading range. Against the U.S. dollar, the peso was trading at these same levels four months ago with a 5% trading range from bottom to top (excluding outliers). Against the U.S. dollar, the Canadian dollar was trading at these same levels three months ago with a 2.6% trading range from bottom to top (excluding outliers). On the biggest single-day of volatility, the day tariffs were delayed for a month right before they were scheduled to take effect, USD/MXN traded through a 4.7% range and USD/CAD traded through a 2.8% range. In other words, both currencies covered their entire range of volatility in one day.

These percentages are large in foreign exchange. The adjustments can be seen in the persistently elevated levels for both USD/MXN and USD/CAD. There is no transitory observation until the volatility dies down and/or the price adjustment itself reverses. In the meantime, I am short USD/MXN out of a belief that economic relations with Mexico are about as bad as they can get. I could of course get proven wrong in due time. On the other hand, I am long USD/CAD because I do not think the market fully appreciates how much weaker the Canadian economy will get as it tries to match the U.S. in this economic warfare. Combined, these two trades are good pair trades where I collect interest income from USD/MXN as I wait. Week-to-week volatility in USD/CAD allows me to execute a few swing trades.

Epilogue

Last week I spent more time understanding the economic theories and frameworks espoused by Bessent. The interview at the Economic Club of New York with Larry Kudlow was educational in that respect. Unfortunately, the recording started after the commentary on tariffs. Minus the cheap shots, the rest of the interview is worth watching and understanding.

Be careful out there!

Full disclosure: long USD/CAD, short USD/MXN

Fascinating! I’m curious about one thing. As someone who has not been able to develop an intuitive feel for currency trading (despite trying): if you’re short USD/CAD and long USD/MXN as a pairs trade, is there an equivalent CAD/MXN trade? What characteristics of the two positions would differ?

I’m actually short USD/MXN and long USD/CAD. If I did CAD/MXN it would be to short it given my claims: 1) I can collect premium from the interest rate differential and 2) the Canadian dollar has not priced in as much damage from economic warfare as the Mexican peso has. However, I prefer splitting up the trade mainly because the dollar pairs offer more flexibility and liquidity. Moreover, I still have to be mindful of country-specific events (like central banks) which may force me to make adjustments. Those adjustments are easier to do when MXN and CAD are not combined in one pair.

I accidentally stated the inverse of your trade, but you answered my question as I intended :-).

[…] that can be the case in the case of tariff inflation.” I critiqued this explanation in “The Sleight of Hand Behind the ‘One-Time Adjustment’ and ‘Transitory’ Tariff Inflation Narr…“. While a tariff can impose a one-time price adjustment, that adjustment embeds higher costs […]

[…] alternative to cash for the conservative part of a portfolio. Even with tariffs creating a “one-time price adjustment higher” in prices, GTIP should get quite a boost in the coming year. Rate cuts from the Fed will […]

[…] Scott Bessent’s line that tariffs are a “one-time price adjustment.” But as I wrote in “The Sleight of Hand Behind the ‘One-Time Adjustment’ and ‘Transitory’ Tariff Inflation Narra…“, for inflation to be transitory, expectations for price levels would need to revert after […]

[…] San Francisco did not provide anecdotes or data on planned price hikes. However, one alarming anecdote came from a business which noted that tariff-related price hikes were not rolled back along with the related rescinded tariff. This inflation “stickiness” is a worrying indicator of how tariff-driven price hikes can cause lasting, cascading price pressures in the economy. […]

[…] if tariffs are hiked all at once in a one-and-done fashion. Otherwise, this reassurance reinforces the same argument Treasury Secretary Bessent made at the beginning of the tariff drama, trauma, and noise. Assuming that long-term inflation […]